Justified optimism – not just hopes – characterizes the world economy 2017-18. Konfliktnivåer has certainly been raised, and the policy challenges should not be reduced. But the protectionist rhetoric is not identical with the practical politics. This is according to SEB’s economists in new Nordic Outlook. The increasing economic activity is globally synchronized. Our high growth forecast for Sweden is lifted further. But when the Riksbank signalled continued full inflationsfokus learn first increase until april 2018 despite the fact that it generally becomes increasingly difficult for central banks to argue for the more extreme forms, including minusränta.

An underlying strength of emerging economies, including China, and a nascent investment cycle balances the political risks around the world. Our positive, truthful picture of the economy continues to be confirmed. GDP growth in the OECD area will be 2.1 per cent this year, slightly higher than in 2016, and 2.2 per cent in 2018. In practice, this suggests the indicators t o m a slightly higher growth than what our forecasts today reflect. Left are, however, major societal challenges, such as economic inequality, population ageing and sectoral job losses due to digitalization and automation.

Trump more pragmatic and less dogmatic – relief for the world

Global economic-political uncertainty is at historically high levels, and becomes of populism and protectionism go hand in hand. Trumponomics has, so far, as expected, proved to be difficult to implement, and the president of the republic has changed its mind several times. The relationship between the world’s two economic superpowers, China and the united states, however, has been improved. World trade shows, after all, a upward trend and seems to be solid overall.

A strong labour market and increased investment, the united states, after a temporary dip in the beginning of 2017, a GDP growth this year at 2.3 per cent, up from 1.6 per cent in 2016, which then reach 2.5 per cent in 2018. The conclusion that “Trumponomics” unable to deliver as much stimulus has been confirmed, which limits the growth by 2017-2018. The USA’s labour market is increasingly tight; the unemployment rate reaches to 4% and lönetillväxten reach up to 3.5 per cent.

China is running in high gear, but Beijing pulls in kreditbromsen

Adjustment processes in emerging economies provides better resistance against u.s. interest rate hikes. High debt and political risks, however, constitute threats. China’s GDP will grow by 6.7 per cent this year and 6.3 per cent in 2018 , with a clear improvement in the manufacturing and construction sectors. Beijing screws, however, to kreditkranen. It reduces future growth but reduces at the same time, the risk of financial imbalances. The other BRIC economies, not least India, confirms the important contribution to the improved global outlook 2017-18.

Even Europe benefit from stronger labor market and the upturn in fixed investment. Eurozone’s GDP growth this year and in 2018, 2.0 per cent and the increase is bredbaserad. The political uncertainty has diminished after the EU-hostile forces so far in supervalåret had modest success, and the German elections will not change the picture. But the threat persists in the longer term. France’s new and untested political leadership faces big challenges and a weak economy forces trade-offs. Italy is also a large financial and political threat to the UNION.

Brexiprocessen is characterized by tough rhetoric and positioning. That Theresa May and Toryregeringen can strengthen its position after the junivalet does not change the image to the likelihood that negotiations will fail increased. British growth is inhibited, thus undoubtedly of political uncertainty during the forecast period.

Changes in the risk spectrum and complicates the argument for an extreme monetary policy

Still, there are good reasons to pursue an expansive monetary policy, but it becomes increasingly difficult to argue for its more extreme forms, for example, minus – and zero interest rates and vast securities purchases. The risk spectrum has shifted: deflationsrisken has declined significantly and the downside risks for growth has slowed. In the US, the Fed continues to make the policy less expansionary through a total of three plus three raises in 2017, respectively in 2018 and reduced holdings of securities. The risk of a procyclical american fiscal policy has been reduced, while financial conditions have become more expansionary in spite of Fedhöjningar. The european central bank has also adjusted the risk spectrum and is expected in september this year to raise the deposit rate by 15 basis points to sek-0.25 per cent, and then decide whether to further reduce the monthly value of debt securities purchased. Low interest rate environment and central banks the presence and valutafokus whole trendlös global foreign exchange market.

Developments in the financial markets is contradictory. Despite political uncertainty and concern for policyframkallade chinese and american recessions are global stock markets near all-time high. In addition, the volatilitetsindex – the so-called “fear-factor” – a 10-year low. With rising profits and a stronger economy, which the stock prices continue upwards. High cost-efficiency, and incipient signs of prishöjningskraft strengthens the image further. Rising long-term rates (approximately 70 basis points during the forecast period) does not prevent a certain amount of further stock market recovery. The price of oil Brent stays at 55-60 dollars per barrel – but with a clear downside risk in a supply – and US-driven market.

Baltic and nordic economies is lifted by the operating environment and the domestic strength

The baltic economies benefit from both improved omvärldsutsikter and domestic drivers – consumption and investment – but they are not without challenges. Estonia’s GDP growth accelerates to about 3 per cent in 2018 but with question marks around the economy’s long-term motivations. Latvia favored by the tax reform, which strengthens the competitiveness and growth potential: GDP growth is expected to be 3.5 per cent in both 2017 and 2018. In Lithuania, pushing exports up growth rates but wage growth may become a problem in the long term. GDP growth will be just over 3 per cent.

The outlook for Finland has been brightened with indicators on flerårshögsta. Industry and investment provides the impetus for growth and GDP growth will be 1.6 and 1.7 per cent in 2017 and 2018. The recovery also continues in Norway , with the help of increased private consumption and investment. GDP growth will be 1.4 per cent per year for both 2017 and 2018. The downside risk of inflation dominates, which gives the Bank reason to keep interest rates low for a long time: the first increase occurs in december 2018. For Denmark’s part is expected to tighter credit conditions turn against the labour market, the GDP growth will be 2.0 per cent this year and 2.4 per cent in 2018.

High and bredbaserad Swedish growth and low inflation creates tension

Sweden’s GDP will grow by 3.1 procenti year and 2.6 per cent in 2018 – some revision of our previously optimistic growth forecast. The indicators speak for even faster expansion, but clear restrictions and bottlenecks on the production side dampens growth. The government is exploiting the very favorable fiscal position – budget surplus of 0.6 percent of GDP per year and public debt falls by 4 percentage points to 38 percent, and adds a valbudget in the fall with expansionary direction. Our main scenario is that you bow to the opposition on a few points, which allows a governmental crisis is avoided before the elections in 2018.

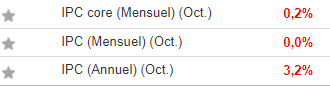

Inflation has come up at a higher and more stable level than in the past but for low wage settlements, the Riksbank difficult to reach the inflation target. A clear fragmented Riksbank also decided in april to extend but reduce the obligationsköpen. In other respects, broadened and strengthened the arguments for a less expansionary monetary policy. That house prices and debt once again started accelerara accentuates how the lack of co-ordination and cooperation between various economic policy actors are becoming increasingly problematic.

Higher resource utilisation, changes of the monetary policy framework and the likely replacement of the governor at the end of the 2017 opening to the end for a reversal of the minusräntan in april 2018 to sek-0.25%. At the end of 2018 is the key interest rate at 0.0 per cent. The crown remains in the short term of 5-10 per cent undervalued but is strengthened to 9.30 and 8.45 against the euro and the dollar by the end of 2017 and to 8,95 respektieve the 7.85 at the end of 2018.

See the filmed summary

Key figures: International & Swedish economy

(figures in brackets are forecasts from the NO February 2017)

Nordic Outlook

Press release (PDF)