Our assessment last week was that the fall was a skrämskott and a false sell signal, but before we returned to our earlier forecast of a rise to 1700 points for OMXS30, we wanted to see a clearer buying interest both in Europe and in Sweden.

We found it difficult to see the logic of the downturn at the end of June, but while a market need power to rise, it may fall of its own weight no matter what it is that triggers the case. When the decline took place during the high volume crime of the important psychological levels we did not dare to dismiss the downturn as just noise of no greater dignity than usual.

We chose to let the picture get clearer, and awaiting with concrete forecasts, and compared with the previous week, the probability increased that there is more to find on the upside, but with the note though that the review period begins in earnest today, Friday.

In the morning, SEB has posted strong numbers, which should affect the entire banking sector is positive, but the real flood of reports beginning in first on Monday and then are inundated with the market of the figures during this week.

It should be noted that any form of analysis whether fundamental or technical temporarily put out of play when new and unexpected information comes on to the table and even the largest and most genomanalyserade companies can quickly move a few percent up or down in conjunction with the figures and the outlook are presented.

In particular verkstadsbolagen have large gains in the back with values that in some cases can be considered as challenging. This means that the prospects will be examined and the market will like to hear clear statements about the positive economic projections for running the courses higher.

We believe that this may be the case, but it is foolhardy to be karsk before the market has shown the cards. Regarding the stock market as a whole, we retain our positive view based on the promising patterns of behaviour, both nationally and internationally.

We had been happy if the u.s. S&P 500 has been boring and moved sideways, but the U.S. exchanges are more positive than expected and the S&P 500 is only a couple of tenths from to pass the ”all time high”. The Dow Jones Index consists of 30 large-cap companies) and with a tad sharper out and tekniktunga the Nasdaq, which is just a couple of weeks experienced a clear the spigot, located above the index in the beat.

The united states

Asia continues to show their prowess and Hong Kong have tvärvänt up to new heights after a fast transient minirekyl. South korea follows in the tracks while Singapore and Taiwan are either in the backwater. Japan is grappling with a listless dollar exchange rate while in contrast, China and not least in India shows obvious strength.

India

Oil continues to be significantly volatile, but starts to after all dig in against on the downside and see de facto for the first time in several months time interesting, with the potential for a movement on the upside. The Russian stock exchange has taken on this and although we are still cautious, so we do not rule out that this market may surprise on the upside.

Gold has held above the 1200 dollars and we are currently not keen to go on the purchase page. Base metals, except nickel, shows, however, continuing positive trends and our favorite in the sector is copper, which started trenda up in what can be a uppgångsfas of more long-term character.

The major exchanges in Europe has been palpable boring with a slight negative slope in more than two months of time. However, we believe that the long-term trend remains positive and that Europe is in a rekylfas of something more protracted character.

The decline during the last days of June, however, was likely a utskakning and the end of this phase. We then got to see a renewed buying interest and this was our specific conditions to be clearly positive about the future stock market performance. Greece, Italy, Portugal and Turkey is striving stubbornly to the north while the broad Europaindexen has reached up to a clearly defined utbudsnivå, which will mean a certain amount of resistance to pass through.

Germany/Europe

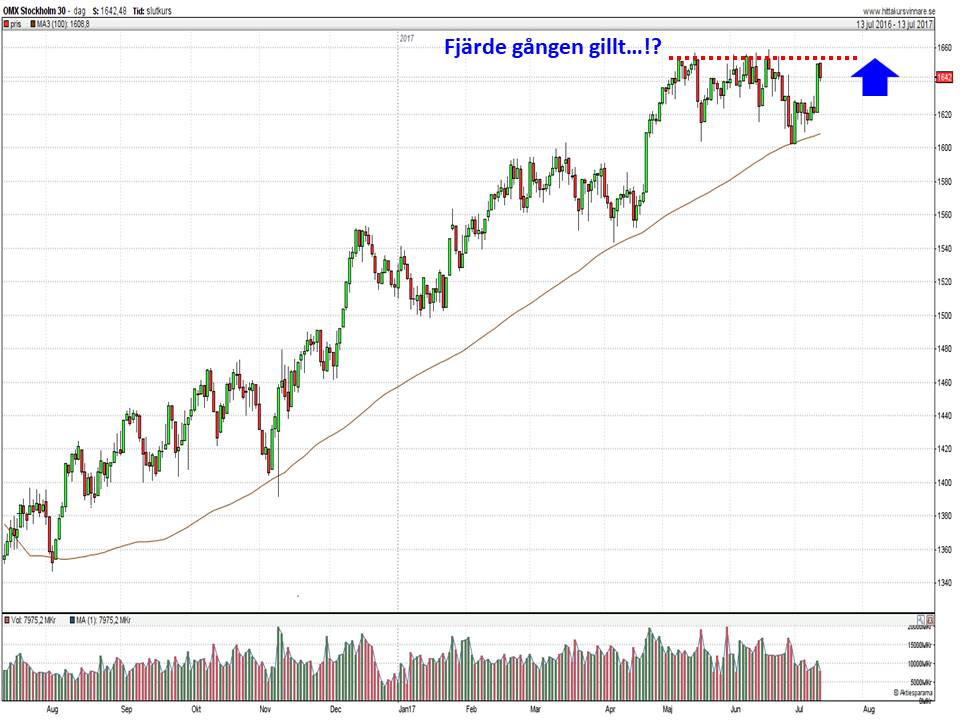

Sweden found itself in a similar utbudssituation during the greater part of the preceding as well as during the first few days of the current week, but on Wednesday passed utbudsnivån – in tune with gains in Europe, USA and Asia – and säljsignalen triggered at the end of June was thus falsifierad. False sell signals tend to be the best buy signals are generated, then they have the ability to quickly and effectively change the mood of the investor community.

With the necessary note though that the upcoming reporting period will not be a disappointment, we see thus a clear possibility that the index (OMXS30) on the fourth attempt successfully pass the high for the year and achieve our målkurs about 1700 points during the summer (now 1647), but pointing with the whole hand, just before the rapportfloden is not professional and there must always be a mental preparedness that even well informed projections can fail. Next week we have the results of the reports and then will come the direction for the stock market trend takes form seriously.

Sweden