Twilio Inc. (TWLO) shares rose over 30% during Thursday’s session after the cloud software company reported better-than-expected first-quarter results Wednesday after the bell. Turnover has increased by 56.5% to $364.86 million, beating consensus estimates by $36.59 million and non-GAAP earnings per share came in at six cents, beating the consensus estimates of 17 cents. The company anticipates revenues of $ 365 million and $ 370 million during the second quarter, which is higher than the $ 323.4 million consensus estimate.

Analysts have reacted positively to the news with a series of upgrades and higher price targets. Bank of America has renewed its first choice of Buy rating and raised its price target from $125 to $195, saying that the work in the house of the wind back will be more than offset weakness in the travel, hospitality, and carpooling. Cowen added that COVID-19 is an “accelerator” for Twilio stock.

Twilio has withdrawn its full-year forecasts due to the impact of COVID-19, but the general trend seems positive for the company’s revenue outlook throughout the year.

TrendSpider

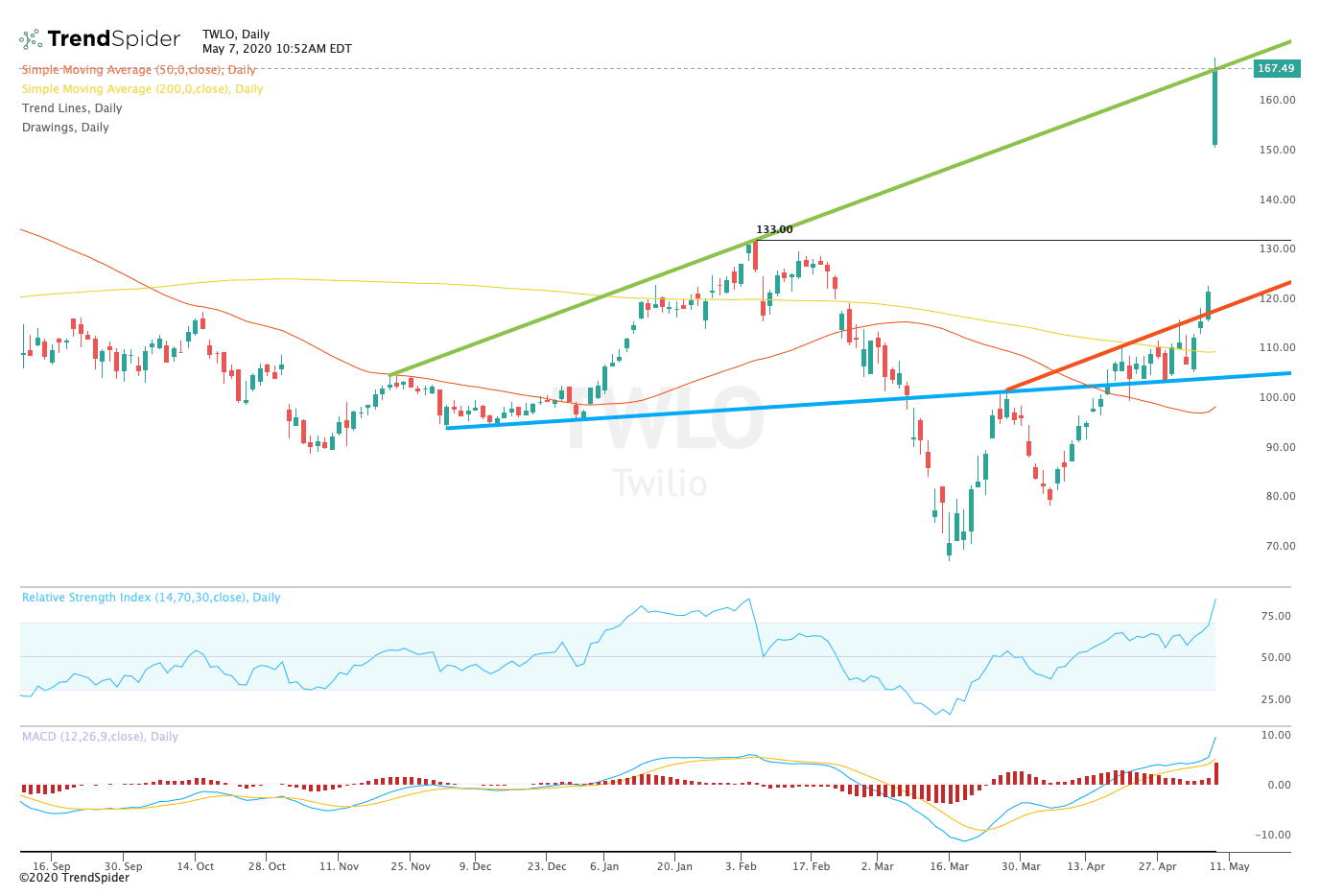

From a technical point of view, Twilio stock broke out of before summits of the fresh 52 weeks highs. The relative strength index (RSI) moved into overbought territory with a reading of 84.00, but the moving average convergence divergence (MACD), has extended its bullish movement to the upside. These indicators suggest that the stock could see a consolidation before resuming its upward movement.

Traders should watch for consolidation between the trend line of resistance of the order of $167.00 and before the vertices of $133.00 over the coming sessions. If the stock breaks down from these levels, traders could see a trend towards the trendline support at $105.00. If the stock breaks out higher, traders could see a fresh 52-week highs.

The author holds no position in the stock(s) mentioned except through the passive management of index funds.

Source: investopedia.com